Bubble Bubble Toil and Trouble

/

We had a perfect recipe for the “abrupt” correction that global asset markets have experienced. A quick look at the factors shows observant investors that caution was necessary leading up to the most recent FED meeting. 1) Leverage as measured by NYSE margin debt released in May showed levels greater than that of 2007 and close to all time highs. This excessive risk appetite can be attributed to an extremely low interest rate environment and low volatility in the broader market. Said simply – leverage is cheap, and the stock market doesn’t decline for long, because of the FED put in the Bond markets… Chart courtesy of DShort @ Advisor Perspectives.

2) Economic indicators have improved in an assymetric fashion in that corporate earnings and growth have been solid, jobless numbers have been improving along with retail sales and consumer confidence, but labor participation rate has a fairly steep negative trend, housing starts were trending positive but experienced a dramatic decline and real gdp has been volatile. Charts via the New York Times and FRED where applicable, sources are cited in chart.

[gallery columns="4" ids="211,207,206,205,204,203,202,201,200,199,198,197"]

3) About that FED put… It has been rumored for some time now that Bernanke and the FED had to begin its exit plan. Market participants have known sooner or later that day would come but volatility had been so low, and debts so large especially with the FED being the largest US debt purchaser that it always seem to be coming next year, or the year after. Well Bernanke slapped the market to attention when he said nothing to contraindicate the rumors that tapering could begin as soon as the 4th qtr of this year.

Whoops! So the mad rush begins as investors have no choice to begin deleveraging immediately. And by investors I don’t mean the average 401k or boutique investment shop. I’m talking about the big boys who literally move markets. These players are leveraged to the hilt and need to begin unwinding interlinked trades across various asset classes. Think carry trades used to speculate in emerging market assets, currencies, and leveraged bets using derivatives.

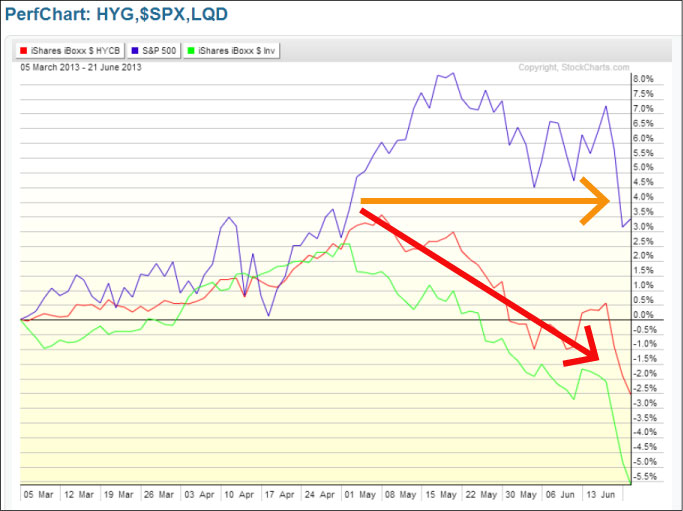

Bond markets have also been flashing warning signs. The chart below represents a high correlation period between the HYG and LQD etf's, and the S&P 500, which act as good proxies for risk appetite especially. Beginning in early May there is a clear divergence between the stock market and bonds.

Couple these factors together and it appears that we have entered a correction phase in asset markets, as some of the “froth” gets wiped away and the players reposition themselves. In future posts I will examine the linkages between shadow banking system, the players involved and the necessity of deleveraging. I will also look for the signal that gave investors the go ahead to get risky in the last round of forced deleveraging.